• Manufacturing signals remain weak

• Jobs and consumer confidence remain positive

• Phase 1 China trade deal gave market a boost

• Overall, GDP growth has slowed but remains persistently positive for now

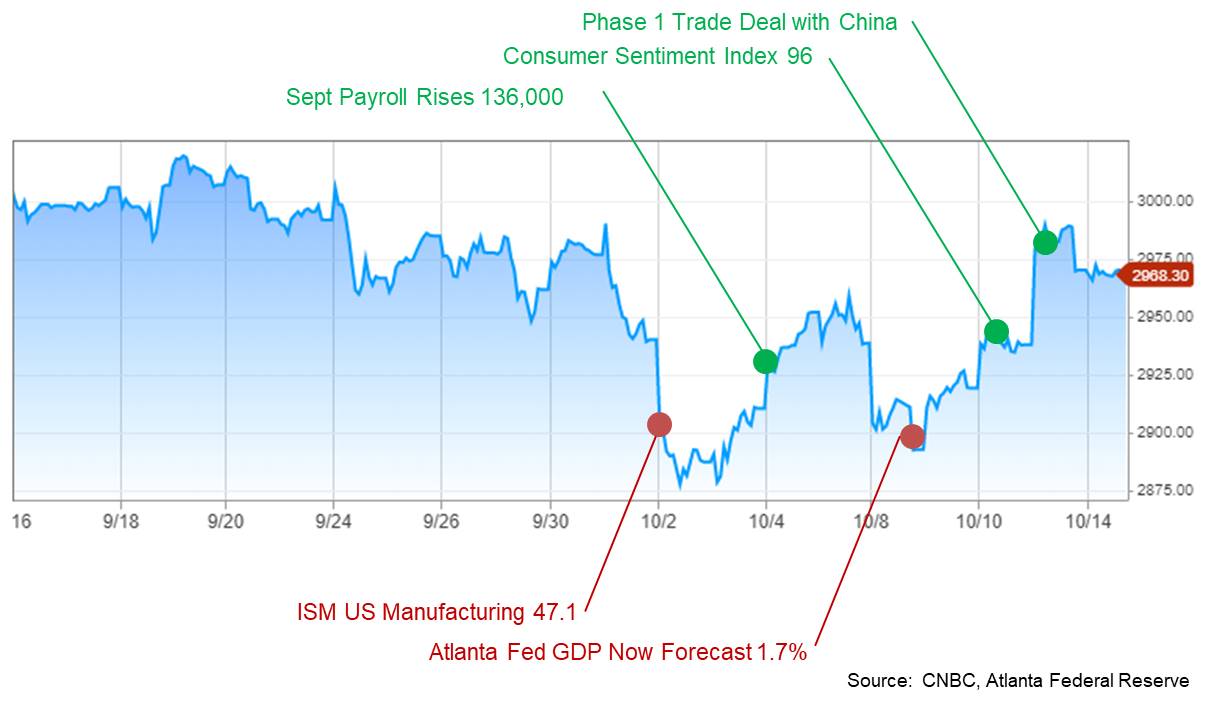

We started October with a flurry of economic reports. The reports have been mixed and the result has been a choppy start for US stocks in Q4. Below, we have a chart of the S&P 500 index with significant economic news data as an overlay.

On October 2nd, the ISM Manufacturing PMI of 47.8 was reported. This is the lowest reading since June of 2009. According the Timothy R. Fiore, Chair of the ISM, a reading of 47.8 “corresponds to a 1.5-percent increase in real gross domestic product (GDP) on an annualized basis”. A reading under 50 is thought to signal a contraction in manufacturing. The last reading we had below 50 was in 2016, in that case we did not enter recession.

The negative ISM reading was followed on October 4th with the latest jobs data. September unemployment fell to 3.5%, a 50-year low. 136,000 jobs were created in the month. This was below forecast of 145,000. The market responded positively to this news.

On October 9th, the Atlanta Federal Reserve updated the GDP Now forecast from 1.8% down to 1.7%. The number is consistent with the ISM data. The reading is below the average trend over the past two years of 2-2.5%.

The weak manufacturing and GDP numbers were offset when the University of Michigan Consumer Sentiment Survey was announced on October 11. The reading of 96 for September is quite positive and beat the estimate of 92. Also, the reading is up from 89.8 in August.

On Friday, the US and China announced phase I of a trade agreement. The first step is a very limited agreement in principle whereby China will increase agriculture purchases and the US agrees to delay implementing previously announced tariffs.

Conclusion

The market’s moves based on the back and forth economic data provide a good illustration for why I wouldn’t put too much focus on market volatility over very short time spans. That said, pulling all of the economic data together helps us form a pretty good mosaic /picture for the economy.

For sure, the economic data is mixed. Based on all of the models I’ve looked at, we have to give a high weight to the jobs growth, the persistent (if not somewhat weaker) GDP growth and low unemployment claims. The US economy is 70% consumer spending and with a strong jobs market and good consumer sentiment, odds of a recession in the very short term are not a given. In fact, I’d put the odds of recession by the end of next year at 25%. The view of slowing growth but no recession is held by Dr Ed Yardeni. Ray Dalio, Bridgewater founder, has put recession odds in the 25% range for 2020 as well. Of course this could all change as new economic data comes in, so we’ll continue to watch it very closely.